This home is located at 23 5th St, SE:

The flier says:

“ENCHANTING Victorian bay-front in a picture-perfect location. Richly-detailed facade sets the tone for the interior–4 rooms deep, each a jewel. Formal LR & DR, Chef’s Kitchen opens to inviting Famkily Rm. 2 fpls! Master BR w/ adjacent luxury Ba, walk-in closet, tranquil rear BR, 2nd full Ba, Office Nook, Improved storage bsmt. Private patio too!”

You can find more info here and photos here.

Well the location is seriously tough to beat but what do you think of the house itself? This 2 bed/2bath is going for $679,500 – sound right?

Recent Stories

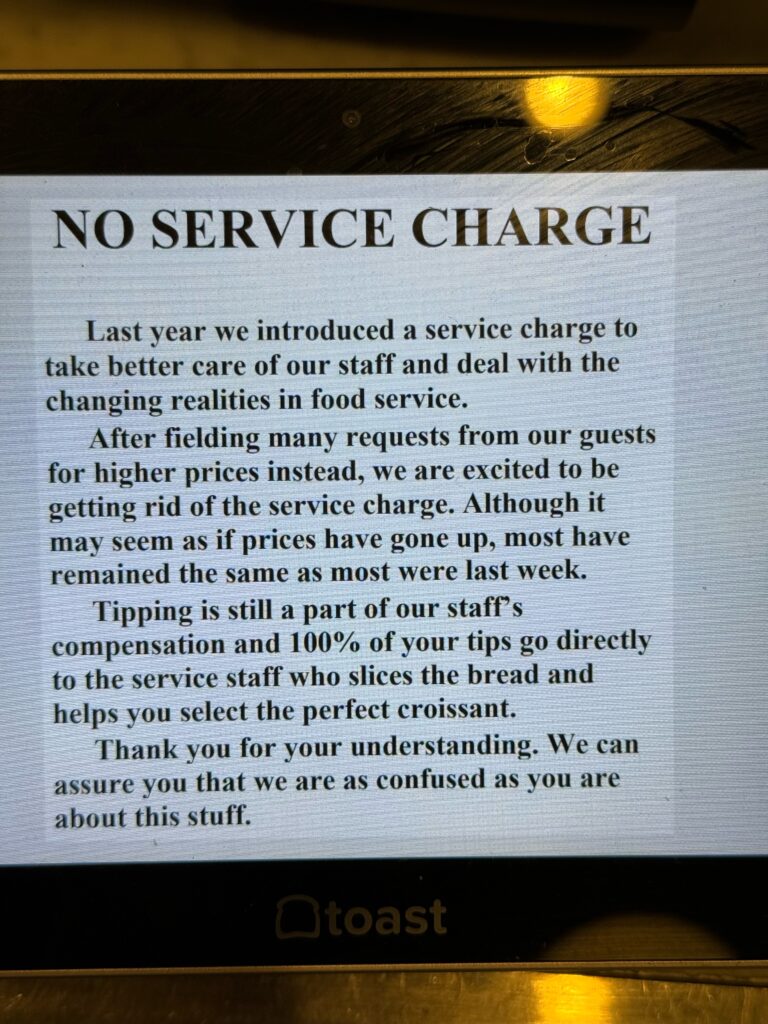

Thanks to Ed for sending: “A very welcome sign on the payment terminals at Bread Furst. I wish more businesses would recognize that transparent prices are what customers want, even…

This rental is located at 1522 12th St NW near Q St NW. The Craigslist ad says:

“Dear PoPville, He has been taking care of my dog for years, and has always been so sweet and kind with him. Mike is the gentlest soul and I literally…

Cleaning out her grandmother’s home, Ellen Rabinowitz discovers a mysterious photograph of a soldier, tucked away in a box of keepsakes. And so begins this sweeping, heartfelt musical about one…

For many remote workers, a messy home is distracting.

You’re getting pulled into meetings, and your unread emails keep ticking up. But you can’t focus because pet hair tumbleweeds keep floating across the floor, your desk has a fine layer of dust and you keep your video off in meetings so no one sees the chaos behind you.

It’s no secret a dirty home is distracting and even adds stress to your life. And who has the energy to clean after work? That’s why it’s smart to enlist the help of professionals, like Well-Paid Maids.

Unlock Peace of Mind for Your Family! Join our FREE Estate Planning Webinar for Parents.

🗓️ Date: April 25, 2024

🕗 Time: 8:00 p.m.

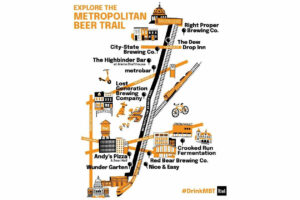

Metropolitan Beer Trail Passport

The Metropolitan Beer Trail free passport links 11 of Washington, DC’s most popular local craft breweries and bars. Starting on April 27 – December 31, 2024, Metropolitan Beer Trail passport holders will earn 100 points when checking in at the

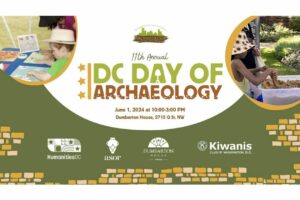

DC Day of Archaeology Festival

The annual DC Day of Archaeology Festival gathers archaeologists from Washington, DC, Maryland, and Virginia together to talk about our local history and heritage. Talk to archaeologists in person and learn more about archaeological science and the past of our