Your condo has a deadline in January 2027. Your board didn’t set it, and probably doesn’t know it’s coming. ONE two understands.

For years, DC condo boards have had room to maneuver on reserves. Underfund a little. Defer the increase. Hope the roof holds one more winter.

The numbers stayed inside the building. The consequences stayed in the future. Most owners never had to think about it.

That just ended. Not because of anything inside your building, but because the rules that decide who can buy a unit in it changed.

What changed

In March, Fannie Mae and Freddie Mac rewrote how lenders judge a condo’s finances. Their guidelines govern most conventional condo mortgages in the country.

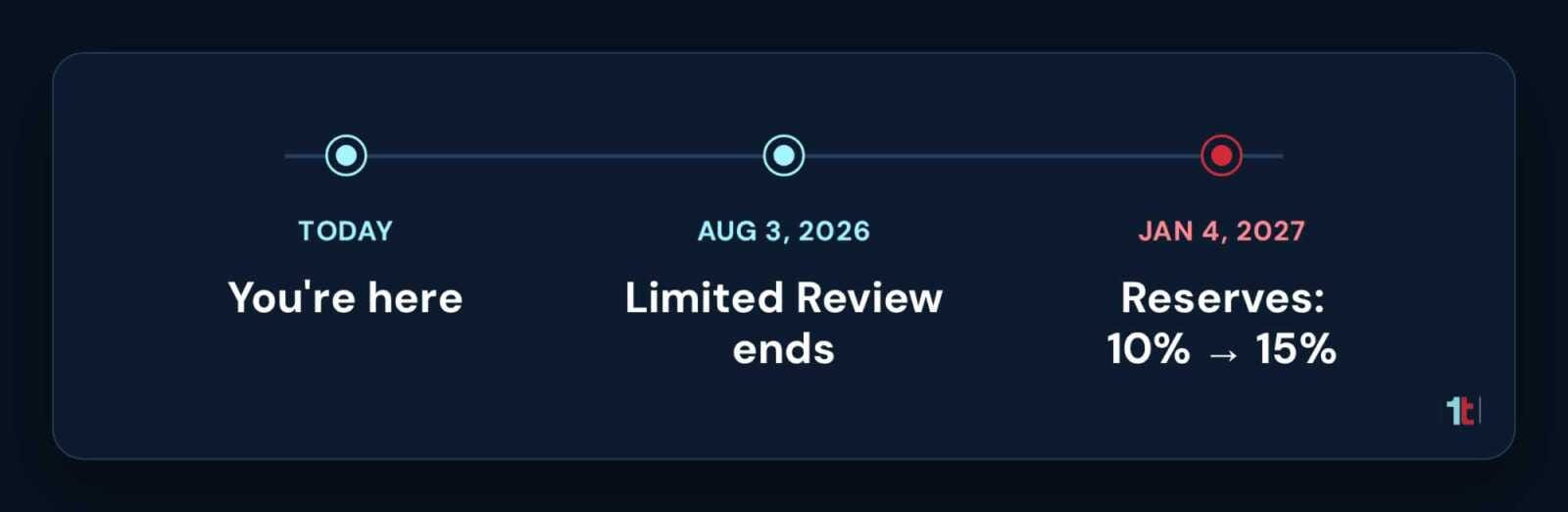

Two dates matter.

Aug 3, 2026. The “Limited Review” shortcut is gone for buildings over 10 units. Every loan now gets a Full Review: budget, reserves, insurance, delinquencies, litigation. No more checking one box and moving on.

Jan 4, 2027. The minimum reserve contribution jumps from 10% to 15% of your budget. For a lot of buildings, that’s a 50% increase in the reserve line.

(A current reserve study can justify a lower number. But 15% alone is no longer a free pass.)

These aren’t laws. Nobody fines you for ignoring them.

But miss them, and your building loses “warrantable” status. Then buyers can’t get a conventional loan for any unit in your building.

Sales stall. Refinances stall. Demand dries up. And values follow.

This is where the music stops

Freeze the assessment. Defer the increase. Lean on a reserve study that quietly aged past three years.

Every board doing that is just moving chairs around the room.

The new rules are the moment someone stops the music. And it won’t happen on your schedule.

It happens the first time an owner tries to sell, and the buyer’s lender opens the books. If the reserves don’t hold up, that owner finds out mid-deal that the building’s finances are now their problem too.

None of that has to be a surprise. That’s the entire reason ONE two exists.

Most boards can’t see it coming

The reserve number is buried in a spreadsheet. The study is in someone’s inbox from three years ago. Nobody has tested the budget against the new bar.

The gap is real. It’s just invisible, until a sale exposes it.

The boards that come through fine aren’t the richest. They’re the ones who see it early and plan a path to 15% over a couple of budget cycles, instead of one panic correction at the deadline.

ONE two gives you that picture

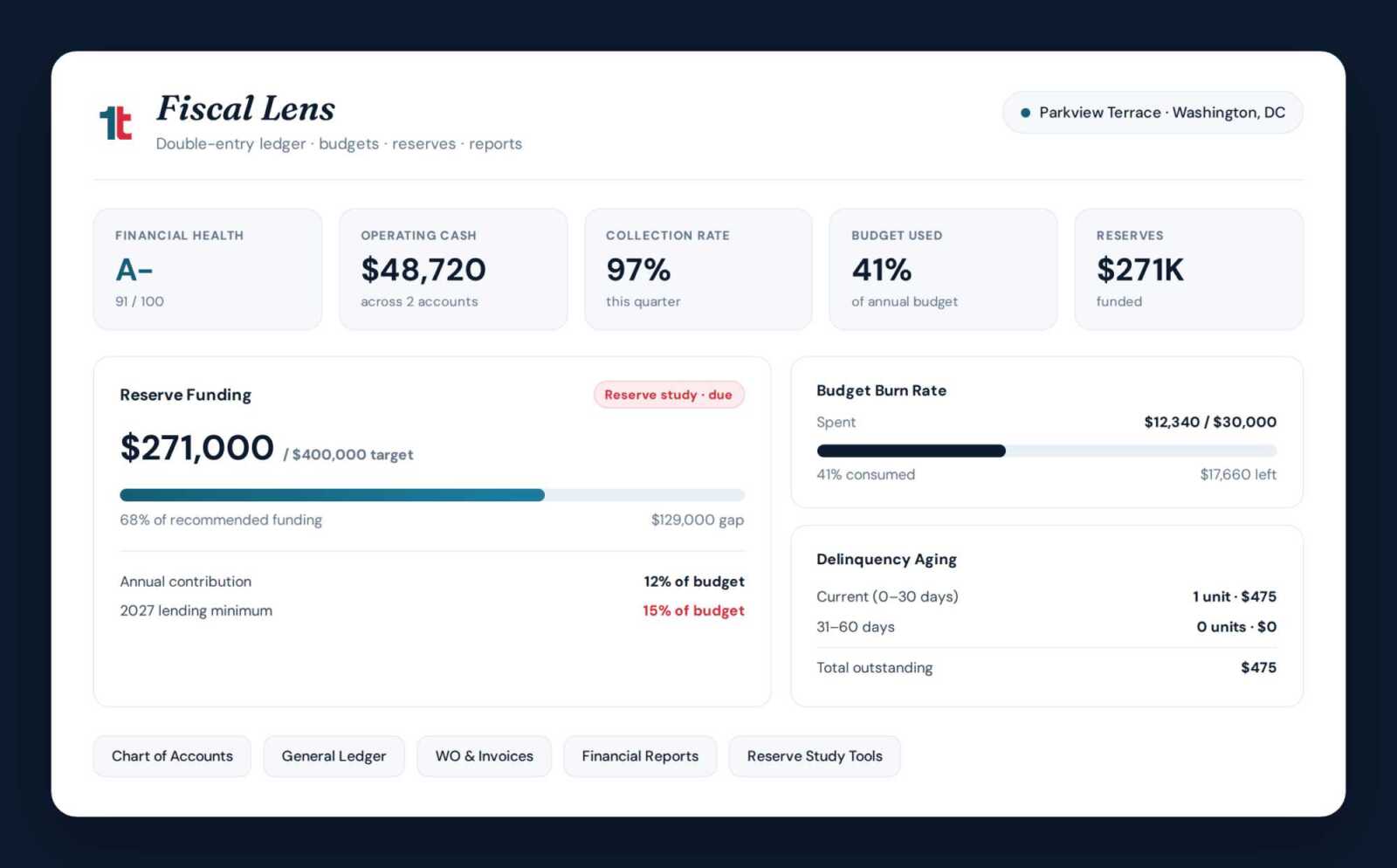

Fiscal Lens puts the whole financial picture on one screen: a Financial Health score, reserves tracked against your capital plan, a live budget burn rate, and delinquency aging.

So when the question is “special assessment, dues increase, or cut costs?”, nobody’s reconciling three spreadsheets on a Tuesday night.

Everyone reads the same live numbers. And you can see which option the building can actually carry.

Then the hard part: deciding

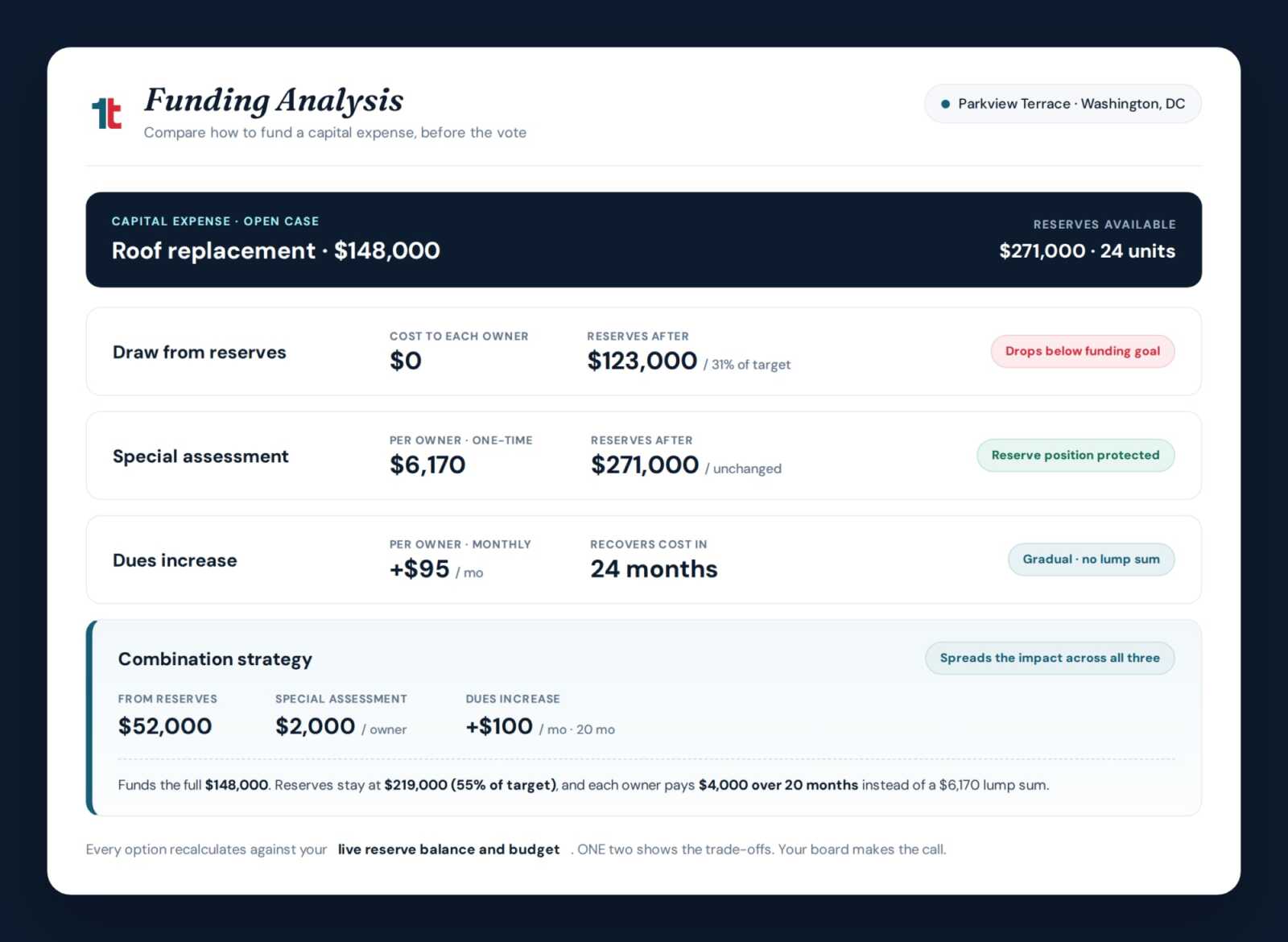

When a real expense lands, a roof, an elevator, a failing boiler, ONE two runs the funding analysis for you.

It lays the options side by side: draw from reserves, special assessment, dues increase, or a blend. What each costs every owner. What each does to your reserves afterward.

The trade-offs are on the table, in real numbers, before the vote.

That’s the difference between reaching for a special assessment because it’s the only lever you understand, and choosing your path because you ran the math.

A board that governs well doesn’t surprise its owners. It protects them. Even the ones who haven’t tried to sell yet.

ONE two is HOA operations software built specifically for DC condos.

ONE two is a compliance-first, made for volunteer boards: homeowners with full-time jobs who shouldn’t need to rely on indifferent property managers to run their building correctly.

Financial oversight, case management, DC compliance, communications, records. Everything built in. Not patched together from spreadsheets and email.

Stop guessing. Start governing. See it in action getonetwo.com.