This is awesome – thanks to a reader for sending:

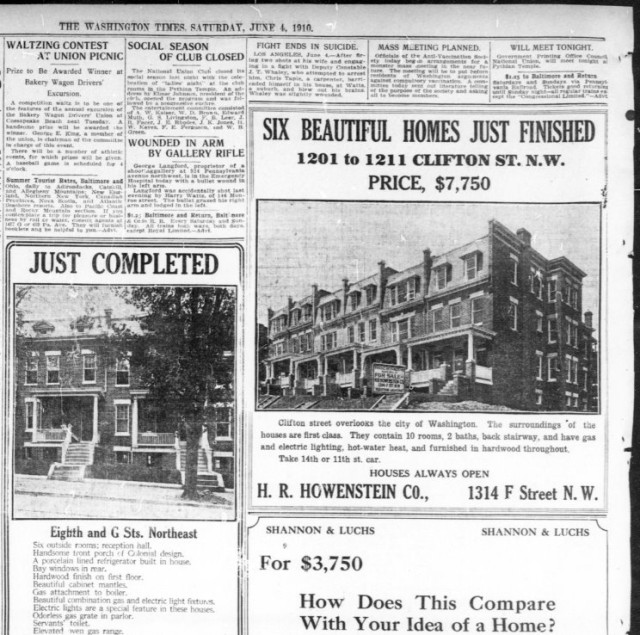

“You listed an apartment @ 1201 Clifton St NW [$1,875/Mo], for a 2 bedroom, 1bath earlier this week. But check this ad from June 4, 1910 from Washington Times. Same place but the whole house for $7,750 and came with gas or electric lighting.

Also 1211 Clifton St, the home on the far left of the original ad just sold this past Sept, 2015 for $1.4 million. So $7,750 in 1910 – $1.4million in 2015, talk about return in your investment!”

Recent Stories

photo by Mr.TinMD From NPS: “The National Park Service (NPS) and National Links Trust (NLT) will rehabilitate Rock Creek Park Golf Course, one of the oldest public golf courses in…

Thanks to John for sending this “Vintage Chrysler 300. 1969?” Sweet City Ride is made possible by readers like you!

Photo by rockcreek Ed. Note: If this was you, please email [email protected] so I can put you in touch with OP. “Dear PoPville, I see the a girl at the…

If you have any animal/pet photos you’d like to share please send an email to princeofpetworth(at)gmail(dot)com with ‘Animal Fix’ in the title and say the name of your pet and…

Unlike our competitors, Well-Paid Maids doesn’t clean your home with harsh chemicals. Instead, we handpick cleaning products rated “safest” by the Environmental Working Group, the leading rating organization regarding product safety.

The reason is threefold.

First, using safe cleaning products ensures toxic chemicals won’t leak into waterways or harm wildlife if disposed of improperly.

Looking for something campy, ridiculous and totally fun!? Then pitch your tents and grab your pokers and come to DC’s ONLY Drag Brunch Bingo hosted by Tara Hoot at Whitlow’s! Tickets are only $10 and you can add bottomless drinks and tasty entrees. This month we’re featuring performances by the amazing Venus Valhalla and Mari Con Carne!

Get your tickets and come celebrate the fact that the rapture didn’t happen during the eclipse, darlings! We can’t wait to see you on Sunday, April 21 at 12:30!

Frank’s Favorites

Come celebrate and bid farewell to Frank Albinder in his final concert as Music Director of the Washington Men’s Camerata featuring a special program of his most cherished pieces for men’s chorus with works by Ron Jeffers, Peter Schickele, Amy

Cinco de Mayo Weekend @ Bryant Street Market

SAVE THE DATE for Northeast DC’s favorite Cinco de Mayo celebration at Bryant Street NE and Bryant Street Market!

Cinco de Mayo Weekend Line up:

Friday, May 3: